Summary

Synapse’s 2024 bankruptcy disrupted millions of users due to financial mismanagement and poor reconciliation of FBO accounts. The collapse exposed risks in third-party banking services, including FDIC insurance limitations and regulatory shortcomings, emphasising the urgent need for stricter oversight, operational resilience, and responsible innovation in fintech.

What would you do if you woke up one morning to find your banking app inaccessible, your funds frozen, and your payments halted? This nightmare became a reality for millions in April 2024 when banking-as-a-service startup Synapse unexpectedly filed for bankruptcy.

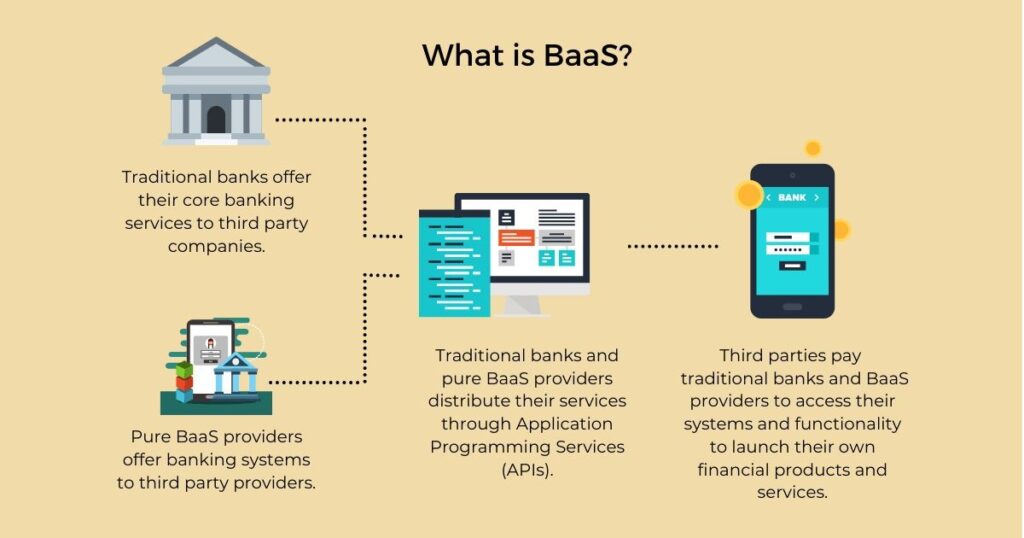

Synapse played a crucial intermediary role, connecting fintech platforms with banks, enabling non-bank entities to offer banking services without obtaining a banking license. Its abrupt collapse left many end-users stranded without access to their funds, underscoring the risks of relying on third-party service providers in the digital banking sector. The situation was further complicated when a proposed US$9.7 million acquisition by TabaPay fell through, plunging Synapse and its stakeholders into uncertainty.

How Synapse Built Trust with Businesses and Customers

Before its collapse, Synapse tried to build trust with businesses and customers by partnering with FDIC-insured banks like Evolve Bank & Trust. The Federal Deposit Insurance Corporation (FDIC) is a U.S. government agency that insures deposits held in member banks, guaranteeing up to $250,000 per depositor in the event of a bank failure. By associating with FDIC-insured banks, Synapse aimed to provide an additional layer of security for customer deposits and minimise risks for end-users. Similarly, Singapore has a Deposit Insurance (DI) Scheme, administered by the Singapore Deposit Insurance Corporation (SDIC), which protects insured deposits held with a full bank or finance company, up to a maximum of S$100,000.

The company also raised US$33 million in a Series B round, backed by prominent investors like Andreessen Horowitz, which bolstered its credibility. Synapse offered a range of financial services through API integration, including payment processing, automated compliance tools, and card issuance. These services enabled businesses to quickly and efficiently build customised banking and payment solutions for their customers, attracting a wide range of clients. These factors allowed Synapse to establish itself as a reliable fintech player, despite underlying operational flaws that would eventually lead to its downfall.

Root Causes of Synapse’s Failure

Synapse’s downfall was rooted in severe operational mismanagement and financial discrepancies. The company’s model involved managing customer accounts across multiple FDIC-insured banks, resulting in significant challenges with reconciling funds.

A key component of this model was the use of “For Benefit Of” (FBO) accounts, which pooled funds from multiple customers into collective accounts held at partner banks. Although commonly used in the fintech industry, FBO accounts come with operational challenges, particularly the complexity of tracking individual customer balances accurately. Poor record-keeping in these accounts can lead to mismanagement of funds, increasing the risk of discrepancies and customer disputes.

In Synapse’s case, outdated reconciliation processes and the lack of real-time visibility into these pooled funds led to significant discrepancies. An estimated shortfall of up to US$95 million in customer deposits was discovered, largely due to the inability to verify end-user balances within these FBO accounts. This shortfall ultimately resulted in the freezing of millions of accounts. The resulting financial turmoil, which included disrupted operations, a loss of customer trust, and increased regulatory scrutiny, was too severe for the company to overcome. Synapse’s collapse highlighted the inherent risks in managing complex fund flows across multiple institutions without robust technological and operational infrastructure.

Immediate Effects on Customers and Businesses

The bankruptcy had immediate and devastating effects. Nearly 10 million end customers and around 100 fintech partners were affected as Synapse’s operations froze. Businesses reliant on Synapse’s banking services suddenly lost access to their funds, were unable to process payments, or connect their financial systems with partner banks, causing widespread disruption across the fintech ecosystem.

For consumers, this incident is a reminder of the importance of understanding where and how their financial assets are managed. It underscores the necessity for transparency in the fintech sector, urging customers to be more vigilant and informed about the institutions handling their funds.

For the fintech industry, Synapse’s collapse highlights the critical need to balance innovation with caution. As the sector continues to evolve, it must do so with a keen awareness of the regulatory requirements and the need for robust risk mitigation strategies. The future of fintech will depend on its ability to adapt to these challenges, ensuring that innovation is sustained safely and responsibly.

FDIC Coverage Limitations in Fintech Failures

The Synapse collapse exposed critical limitations in FDIC insurance coverage for fintech companies. While Synapse partnered with FDIC-insured banks, the insurance does not extend to non-bank entities like Synapse, which act as intermediaries between consumers and banks. As a result, many customers with funds in Synapse’s FBO accounts were left unprotected. Although some consumers might eventually recover funds through bankruptcy proceedings, the process can be lengthy, highlighting a gap in protection for customers of fintech platforms. This situation underscores the need for clearer regulations and consumer protections in the fintech industry, ensuring that customers do not face similar risks in the future.

Regulatory and Industry Implications

Following the fall of Synapse,the Federal Reserve and FDIC have emphasized the need for enhanced regulatory frameworks and tighter controls over fintech operations. There is a strong emphasis on robust risk management practices, which are central to their strategy to prevent similar financial disruptions in the future. Specifically, the FDIC has been advised against allowing fintechs to misleadingly claim deposit insurance coverage. As noted in the Consumer Federation of America’s report, “The FDIC should not permit any fintech to claim it has deposit insurance if funds are held in ‘for benefit of’ (FBO) accounts where ledgers cannot verify end-user balances at all times.” This push for stricter regulation highlights the urgency of protecting consumer funds and ensuring the stability of the digital financial services ecosystem.

Global Perspectives in Digital Banking: The Success of Standard Chartered’s nexus in Singapore

The failure of Synapse, caused by poor operational management, raises important questions about the need for proper regulation and stability in fintech. In contrast, Standard Chartered’s Nexus in Singapore shows how strong internal controls, coupled with strategic partnerships, can help avoid risks. Nexus allows consumer brands, digital platforms, and e-commerce companies to offer banking services directly to their customers. This BaaS model provides the infrastructure needed for companies to easily integrate financial services like deposits, loans, and payments into their platforms, while relying on Standard Chartered’s banking expertise and regulatory compliance.

Although Synapse also relied on a BaaS model, its downfall underscores the importance of not just partnerships, but also maintaining robust operational practices and stringent regulatory oversight. Nexus’s success highlights how combining strong internal controls with effective partnerships can offer valuable insights for both consumer-facing and infrastructure-focused fintech models.

The collapse of Synapse underscores a critical lesson for the fintech industry: innovation alone is not enough. Operational integrity and strict regulatory compliance are essential to prevent financial disruptions. Moving forward, the industry must focus on building resilient systems that ensure consumer protection and financial stability. The Synapse failure will likely prompt fintech companies and regulators to implement more stringent oversight and risk management practices, shaping a future where trust and stability are paramount. Ultimately, the success of fintech will depend on its ability to innovate responsibly while safeguarding the financial well-being of its users.

Disclaimer: The views and opinions expressed in this article are solely those of the author and do not reflect the official policy or position of the National University of Singapore (NUS) or the NUS FinTech Lab.